Rates/CEO confidence and some good earnings anecdotes

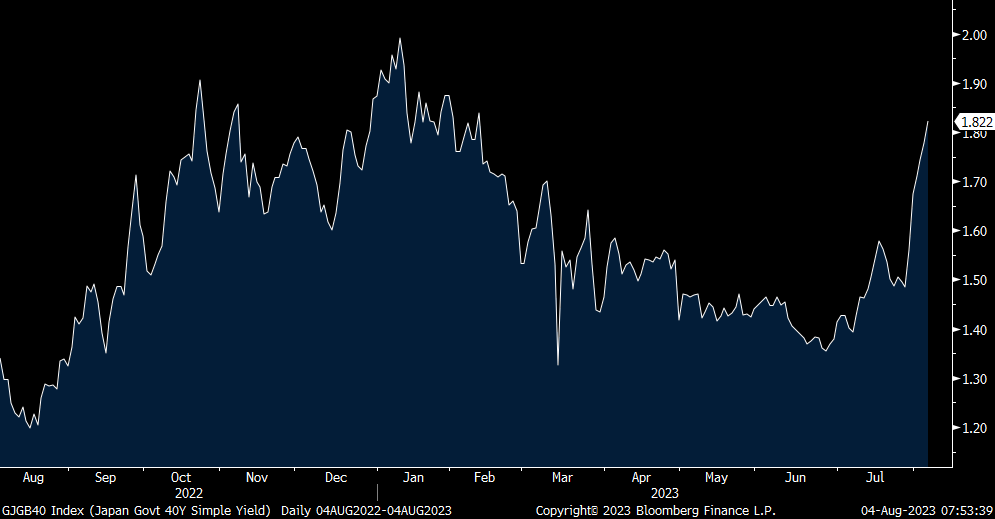

Bond selling continued overnight in Asia and into Europe's trading day and why US yields are around their highs of yesterday. The 40 yr JGB yield rose for the 6th straight day, up another 5 bps to 1.82%, the highest since April. The German 10 yr bund yield is touching the highest since March. The issue here, outside of the obvious jump in rates on top of massive sovereign debt and the rise in the cost of capital for everything else too is that we know central banks have direct control over short term rates but only via QE can they manipulate longer end yields and of course QT is going on and the BoJ has loosened its reigns on QE.

The relief needed at least in the very short term is some real notable economic slowing or at least today, a soft US payroll report. That said, economic slowing would further reduce tax receipts and further deteriorate government finances. No free lunch unfortunately now.

40 yr JGB yield

Here are some of the details from yesterday's quarterly CEO Confidence survey where it rose 6 pts to 48 q/o/q though still below the breakeven level of 50. They said, "Despite the brighter outlook, most CEOs still anticipated an economic downturn ahead. In Q3, 84% reported that they are preparing for a US recession over the next 12-18 months, compared to 93% in Q2. That said, the vast majority continued to expect a short and shallow US recession, with just 4% now expecting a deep US recession with major global spillovers, down from a high of 13% in Q4 2022. Meanwhile, the proportion of CEOs expecting no recession at all climbed steadily from 2% in Q4 2022 to 17% in the latest survey."

Keep reading with a 7-day free trial

Subscribe to The Boock Report to keep reading this post and get 7 days of free access to the full post archives.